As the environmental hazards caused by climate change grow more severe and frequent, increasing attention is being paid globally to the need for genuinely sustainable business practices. Although the financial sector is considered a smokeless industry with little to no direct impact on the environment, it plays a critical role in driving low-carbon economies worldwide. The second facet of CTBC Holding's TRUST approach is "R", referring to "responsibility". We acknowledge the responsibilities that we have as a corporate citizen—an acknowledgment that has inspired and informed our "Green Policy, Green Future" commitment. Our efforts in this area start with reducing our own energy use and carbon footprint by developing new green products and strategies and engaging in sustainability-centered initiatives with our customers and employees alike.

Our environmental sustainability policies

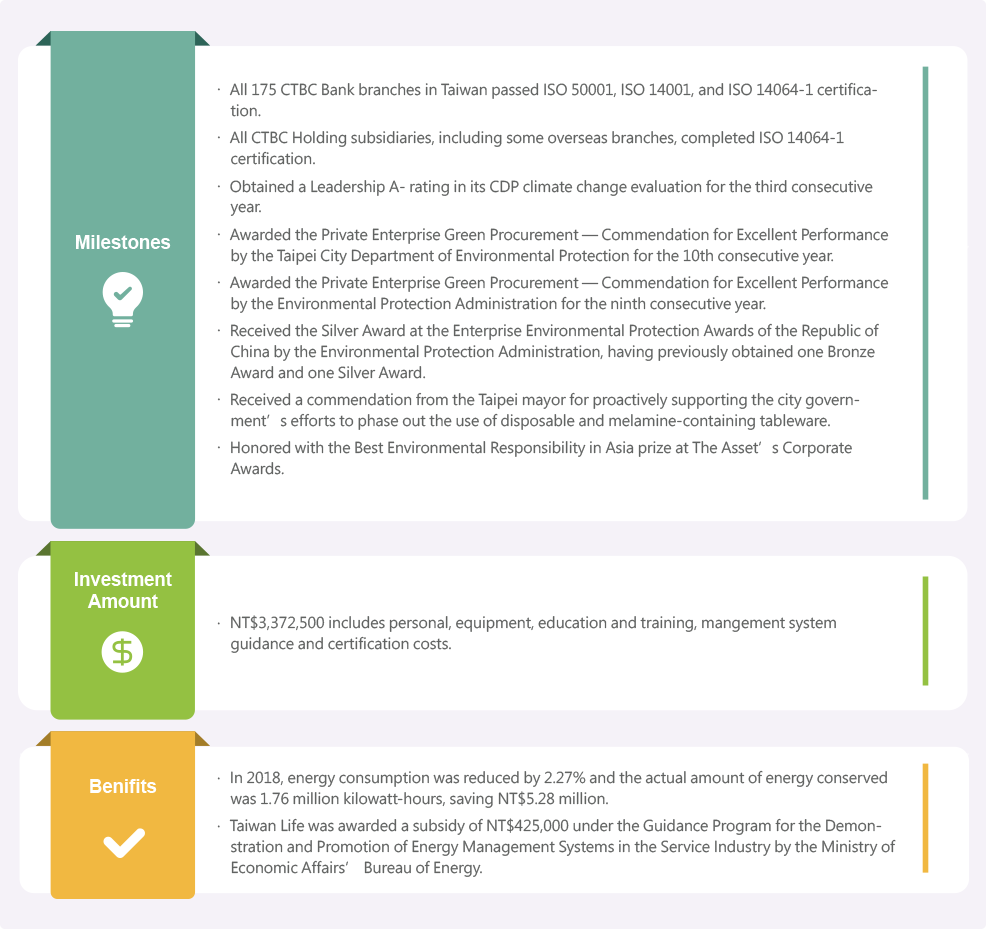

Energy conservation and carbon reduction

Energy conservation, carbon reduction, and environmental sustainability are core concepts for which the Company continually advocates. CTBC Holding was one of Taiwan's first signatories to the CDP climate change project. It has responded to CDP questionnaires consistently since 2012, and has obtained an A- rating in the leadership evaluation of the Climate Change Questionnaire for three consecutive years since 2016.

Driving performance through energy management

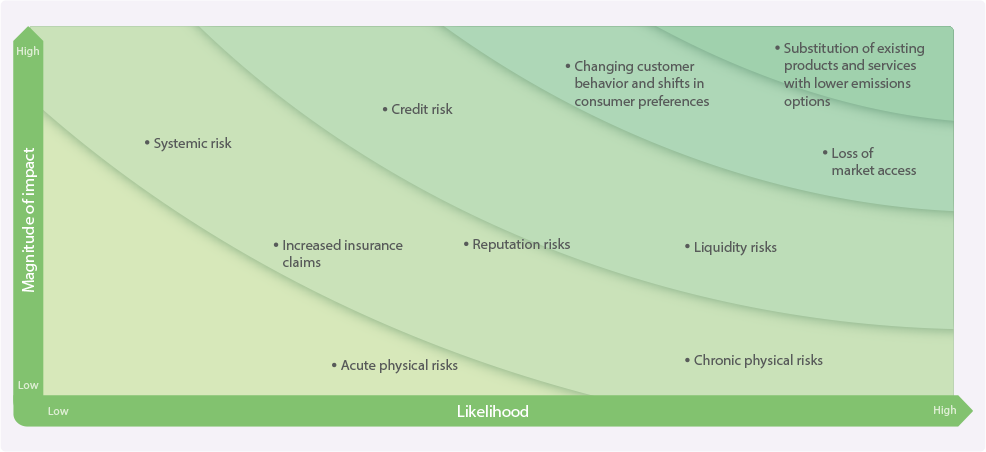

Task Force on Climate-related Financial Disclosures

After the Task Force on Climate-related Financial Disclosures (TCFD) was established in 2017 by the Financial Stability Board, CTBC Holding started to voluntarily adhere to TCFD-developed disclosures in detailing the impact of climate change on the Company's financial situation as well as its future response strategies.

Clinate change risks matrix

Types of major climate change-related risks

| Risk type | Investments and loans | Project financing | Asset management | Insurance |

| Risk type | In the event that an investee encounters climate change-related risk that results in reduced revenue and profits and a lower share price, the performance of the investor and thus CTBC Holding's profits may be negatively affected. | if large-scale financing is given to climate-sensitive industries, mass breaches of contract will cause severe fluctuations in the interest rate, the exchange rate, and other market risk factors for the global market. | If CTBC Holding is involved in climate change-sensitive industries or if debts, funds, or other products are in an industry that may be highly affected by climate change, changes in the enterprise's revenue may be exacerbated, uncertainty may be created in debt repayment and profitability, and the performance of our investment may be negatively affected. |

Climate risks are a constant and irreversible factor with respect to real estate investment. For example, extreme rainfall, exacerbation of the urban heat island effect, and other factors will impact real estate investments.

If the Company's leases cannot be continued due to interruption to its real estate tenancy business, or if the real estate held by the Company is damaged by a natural disaster, negative effects, such as inceased operating costs, may result. |

| Transition | If investments in climate change-sensitive industries face regulatory or low-carbon technology transition pressures and are unable to perform product upgrading and industrial transformation in due course, profitability and investment value may decrease and these investees may be included on the negative lists of consumers investors. | If the customer is in an industry that is highly dependent on fossil fuels, is highly pollutive, has high carbon emissions, or is greatly impacted by climate change, operating profits may be affected by factors such as changes in energy regulations and increases in carbon prices, possibly causing insolvency. | The investment market evolves quickly, with numerous new products for investors to choose from. However, a downward market revision will affect the decision-making of investors, to which the Company must have products ready in response. | If the Company fails to actively research the development and pricing of products that may be affected by climate change risks, it may lose related markets, negatively affecting its revenue. |

| Physical | Real estate guarantee products are an important source of creditor protection; natural disasters causing depreciation or liquidity issues for collateral will erode the capital of the Bank. |

Before we approve project financing, the customer is required to purchase insurance for its production equipment. This enables it to claim compensation for equipment damaged by natural disasters, thereby minimizing our Bank's potential losses.

When the compensation is insufficient to cover all the losses, the Bank judges whether the equipment damage will likely have a significant impact on the overall operations of the creditor, according to the degree of equipment damage, and whether this will pose related risks. |

Natural disasters may cause the closure of the local stock exchange, causing loss of business. | Natural disasters may cause an increase in claims by policyholders, negatively affecting the Company's revenue. |

Management of climate change-related risks

|

Management

orientation |

Investments and loans | Project financing | Asset management | Insurance |

| Operations | Before finalizing an investment in a climate change-sensitive industry, we place particular emphasis on evaluating the environmental, social, and governance aspects of the potential investee company. Through seminars, symposiums, and interviews with upstream and downstream companies and business teams, we strive to understand the industrial and operational impacts of climate change on the potential investee. Investment units consider all such impacts and make an investment decision accordingly. | Environmental protection-related field visits are actively conducted and environmental impact assessment reports are reviewed for domestic industries and large-scale developments that are highly sensitive to environmental risks, thereby ensuring effort in and commitment to projects' environmental friendliness. Regarding our overall operations, long-term climate change risks are reduced by adopting to the Equator Principles, to which we are an EPFI. | At present, when undertaking underwriting, listing, and other business, in addition to reviewing future business conditions, field surveys are also conducted, such as by visiting plants to inspect their actual operating conditions, in order to ensure the Company's fulfillment of due diligence. In the future, investment will be focused on the R&D of climate-related financial products in accordance with industry characteristics and customer demand. | In response to the business opportunities posed by climate change, CTBC Holding has started assessing operations related to climate-related risks, analyzing the degree of impact of climate change on existing customers, carrying out R&D on new forms of insurance that are related to climate change, and improving the method to reduce damages incurred by policyholders from climate change disasters in existing product portfolios. With regard to seeking new opportunities, the recent developments of companies in the same industry and of market demand will be referenced and products such as new forms of weather insurance, agriculture and fisheries insurance, electric vehicle insurance, and more favorable terms for green projects will be launched, thereby increasing the Company's revenue and market share. |

| Financial | If an investee is an enterprise that may be highly impacted by climate change, consideration will be given for early disposition of the invested segment before the occurrence of such an impact in order to reduce the indirect financial impact on the Company. As investment in climate change-sensitive industries may cause the Company's revenue to decrease or asset value to depreciate, suggestions and support will be provided to the relevant investees in the establishment of climate change response units to promptly assess the R&D of new technologies and thereby reduce or prevent any impact on the Company at the revenue/asset end. In addition, suggestions will be made to investees regarding R&D investments in emerging technologies and low carbon product roadmaps will be announced promptly. | Following the Company's signing on to the Equator Principles, the credit process and organizational structure will be adjusted and manpower costs, external appraisal expenses, annual fees, business travel expenses, case-tracking expenses, and employee training expenses will increase. Approximately eight credit cases per year are applicable to the EPs and it is estimated that expenditure on the abovementioned costs will increase by an average of NT$8 million every year. | We are responding proactively to climate change—both its harmful effects and opportunities—in a manner that will benefit the development of the green energy industry, including by actively assisting in the listing of companies in the field. | Attention is focused on the development of large-baseload renewable energies such as biomass and geothermal energy. Renewable energy certificate market transactions are expected to occur in the future and the establishment of smart meters and microgrids is also being pushed forward because of the problem of intermittent supply that can come with green energy plants, with these efforts helping increase revenue. |

| Strategy | CTBC Holding will reduce investments in industries that may be adversely affected by climate change and will increase investment in industries that are positively affected by climate change. | The Company will clearly explain the purpose of the Equator Principles to its customers to help them understand the importance of ESG and of implementing responsible lending. | Because of the particular characteristics of the industry, most customers currently select investment from a strictly profit-oriented position. Upon evaluation, we believe that customers will not be affected by climate change in the short term but that we should nonetheless plan to launch specific financial products in order to expand the sources of profit in the future. | A consulting company will be invited to perform diversified assessments based on the natural disaster model. In order to diversify self-retained loss risks regarding typhoons, floods, and other natural disaster-related products, a reinsurance guarantee has been purchased every year for 100-year typhoons and floods. The relevant typhoon- and flood-related insurance products will be underwritten in accordance with the underwriting guidelines in order to prevent the risk of accumulating overly high amounts of insurance coverage for a single area, and relevant reinsurance will also be arranged to diversify risk. |

Green finance and services

Rates of CTBC Bank customers who have performed online transactions

| Transaction | 2018 | 2017 | 2016 | 2015 |

| Foreign exchange (%) | 68 | 71 | 69 | 65 |

| Mutual fund investment (%) | 60 | 58 | 58 | 58 |

| Interbank transfer (%) | 68 | 61 | 59 | 54 |

Carbon reduction benefits of CTBC Bank credit card electronic billing

| Item | 2018 | 2017 | 2016 | 2015 |

|

Accounts with electronic

credit card billing |

1.7 million | 1.44 million | 1.18 million | 1.01 million |

| Sheets of paper saved | 56.2 million | 47.59 million | 38.98 million | 33.4 million |

| Reduction in carbon emissions (Tons of CO2 equivalent) | 513 | 434 | 356 | 305 |

- With an average monthly e-billing rate of 92% recorded.

- One sheet of A4 paper produces 7 g of CO2 and one bill consists of about three sheets of A4 paper. (data source: https://cfp.epa.gov.tw/EN)

- https://www.twmf.org.tw/Common/ShowImage.ashx?fid=dfcbfe18-16dd-417d-a8cd-53bc4accc898

ATM service replacement rate and paperless credit card applications benefits

- Replacement rate = deposit / withdrawal amount ÷ total number of ATMs.

- One application form consists of approximately 1.5 sheets of A4 paper, and one sheet of A4 paper produces 7 grams of carbon dioxide.

Microfinance

CTBC has always been committed to being a caring enterprise. “Caring” is a core brand value and one we act on y delivering tangible care and support to those who most need it. One way in which we do this is by offering microfinance products and services as means of helping underprivileged families. Through the five major avenues of loans, insurance, credit cards, trusts, and compassionate service, we aim to harness the financial sector's influence to eradicate poverty and create a truly sustainable future.

Microfinance products

| SME loans | For CTBC Bank's loans to SMEs, emphasis is placed on establishing local branches and using them and their advantages to manage SME customers through specialized units. In recent years, to improve these services and better meet the diverse needs of our borrowers, we have provided an ever more comprehensive range of financial services such as financial planning, cash management, enterprise salary allocation, and financial consulting, with a focus on integrating the needs of businesses and business owners in accordance with their business life cycles. As a result of this approach and the Bank's overall action plan, the compound annual growth rate of SME loans in the past three years was approximately 13%. We are committed to developing this customer base further in the future and cementing our position as the best partner to SMEs. |

| Microloans |

|

| Microinsurance | Taiwan Life, in support of a government push, offers microinsurance products for individual, collective, and group insurance. In addition to directly targeting these products to disadvantaged groups, donations are also made to the insurance premiums of these groups in order to further expand the scale and scope of coverage. |

|

Charity credit

cards |

|

| Trust services for elderly and disabled persons | To ensure that the assets of people with physical and mental disabilities are protected, and to avoid asset misappropriation or fraud, we maintain a service that facilitates the establishment of trusts with dedicated funds for various purposes. Specifically, these can be used to ensure the payment of the future care and medical expenses of people with disabilities. |

| Charitable trust | We assist clients in planning and establishing public trusts. This helps trustors to operate and participate in public charitable activities and give related donations through the trust system, thereby giving back to the community by assisting disadvantaged groups and obtaining maximum benefits from limited resources. |

|

Customer assistance

in debt management |

In addition to providing repayment schemes based on the circumstances of customers during the debt management process, we provide assistance for disadvantaged debtors. Specifically, we promote products and services being sold by debt management customers so as to increase their income, refer them to social assistance organizations, and provide donations and assistance to support their children. |

Microfinance services

| Physical disabilities |

|

| Remote areas | CTBC Bank ATMs provide more than 80 services—the most of any machines in Taiwan. As well as performing traditional banking services, the machines can be used to make various payments, such as phone bills, insurance payments, and charitable donations. In addition, an interbank deposit function was launched in October 2015. Diverse ATM services and the application and transaction services accessible online are a game-changer for people in remote areas, for whom traveling to a bank branch may be difficult. |

| Older peoplee | In response to Taiwan's rapidly aging society, CTBC Bank has set up "care counters" at 85 branches since 2015 to provide older customers with services while seated, including a free form-filling service and the ability to conduct transactions verbally. |

| Migrant workers | CTBC Bank launched U Remit, an ATM foreign currency remittance service to help migrant workers send their earnings from Taiwan to their home countries. By providing a safe alternative to the commonly relied upon underground exchanges, U Remit protects the security and interests of remitters. |

| Smart text customer service | We provide text-based services to people for whom verbal communication is inconvenient, such as those the hearing impaired. These, in conjunction with automated smart service mechanisms, provide this group of customers fast and convenient financial support. |

Responsible investment

On Jan. 23, 2019, CTBC Bank became an official Equator Principles Financial Institution. In addition, the Bank is continuing to abide by the United Nations' Principles for Responsible Investment and Principles for Sustainable Insurance as well as the Taiwan Stock Exchange's Stewardship Principles for Institutional Investors, and is supporting the government's "5 plus 2" industrial innovation plan.

Since Taiwan Life first took action in response to government calls for support of green energy development, in 2014, and the "5 plus 2" industrial plan, in 2017, it has made investments totaling NT$1.89 billion. These investments include three solar energy-related projects, one natural gas power generation project, one waste treatment company, and one sewage treatment plant, with an estimated annual reduction in carbon emissions of 830,000 tons. In 2019, we expect to invest in either one or two additional solar energy-related projects and one wind power-related project, and our total investment is expected to range between NT$1 billion and NT$2 billion.

Taiwan Life green investment

| Period | Company | Sector | Investment amount (NT$ hundred million) | Estimated annual power generation (10,000 kWh) | Carbon reduction (metric ton) | Carbon reduction effect as a number of Da'an Forest Parks (Note 1) |

| 2014 to present |

Star River

Energy Company. |

Solar power generation | 1.776 | 5,843 | 30,850 | 117 |

| 2015 to present | Star Energy Co. | Natural gas power generation | 1.71 | 151,000 | 604,000 | 2,309 |

| 2016 to present |

Star Shine

Energy Co. |

Solar power generation | 9 | 25,327 | 133,980 | 512 |

| 2017 to present | Whole Sun Power Energy Co. | Solar power generation | 3.27 | 11,740 | 62,105 | 237 |

| 2018 to present | Whole Sun Power Energy Co. | Sewage treatment | 3.18 | - | - | - |

- Da'an Forest Park, located in Taipei City, covers an area of 25.894 hectares; the calculation of the equivalent carbon reduction effect is based on an annual carbon uptake of 10.1 tons per hectare, as stated in the 2015 National Greenhouse Gas Emission Inventory (data source: http://unfccc.saveoursky.org.tw/2015nir/uploads/06_content.pdf).

- The estimated annual power generation is calculated according to the relevant parameters of the investment proposals.